Posted inVoucher Templates

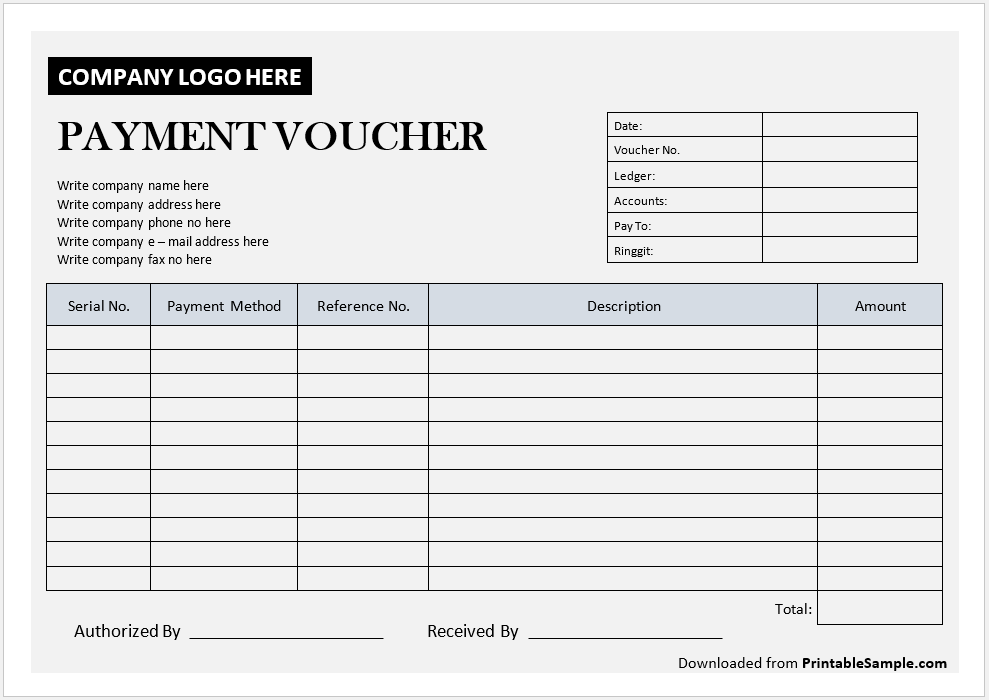

12 Free Printable Payment Voucher Templates

There are no assets with a higher inherent risk of theft than cash. Because of this, it is important to have strong internal controls in place to protect cash payment receipts. The cash payment receipt from the seller to the buyer or the customer or the client. It is important to be very careful while filling in the receipt as any miscalculation can lead to a dispute that spoils the reputation of that very person. The cash payment receipt has all the details of a customer that he/she bought from you. It is for the record-keeping purposes. So, the cash…